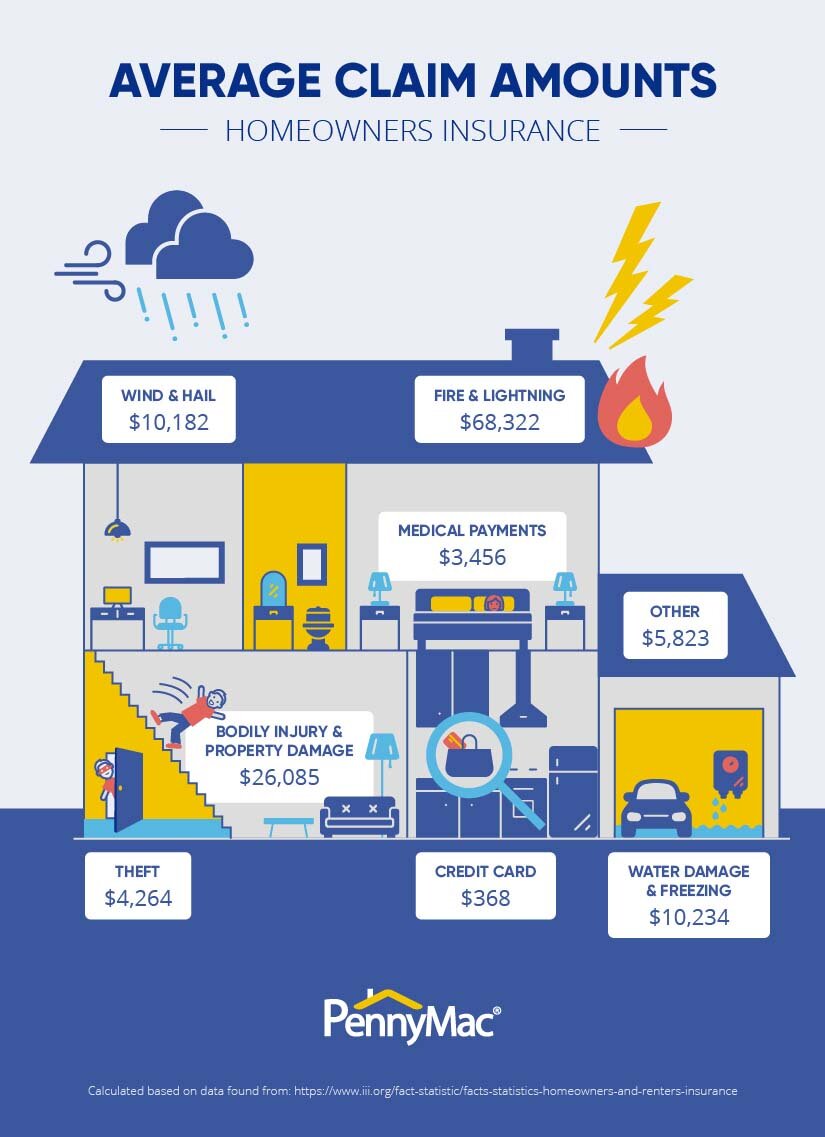

Understanding Your Insurance Property Estimate

Insurance property estimates can be difficult to decipher, especially if you haven’t had experience dealing with them before. Whether it’s roof damage from a hail storm, gutter damage, or siding issues we are here to help you figure out what exactly that means for your home. Here is a guide to help you better understand the estimate given to you by your insurance agent. Homeowners insurance policies generally cover destruction and damage to a residence's interior and exterior (for example: weather damage to your roof or other parts of your exterior.), the loss or theft of possessions, and the homeowner’s personal liability for harm to others.

Common units of measurement used:

EA- each

LF- linear foot

SF- square foot

SY- square yard

CF- cubic foot

CY- cubic yard

SQ- square

HR- hour

DA- day

RM- room

Important information on your estimate cover sheet:

· The contact information of your claim professional

· Your claim number

· The type of coverage under your policy, including the applicable deductibles and policy limits.

· Your estimate may include policy sublimit for specific items, such as money. Each sublimit has a unique ID tag. That ID tag will appear next to any line item that is subject to the sublimit.

Your estimate details:

This is where the details about your lost or damaged property can be found.

· Description: Details describing the activity or items that are being estimated.

· Quantity: The number of units (EA, SF, LF, etc..) for an item.

· Unit: The cost of a single unit.

· Replacement Cost Value (RCV): The estimated cost of repairing a damaged item or replacing an item with a similar one. RCV is calculated by multiplying Quantity x Unit Cost.

· Age: the age of the item that was lost or damaged.

· Life: the items expected life assuming normal wear and tear and proper maintenance.

· Condition: The items condition relative to the expected condition to an item of the same age. (New, Above Average, Average, Below Average, Replaced)

· Depreciation %: The percentage of the loss of value that has occurred over time based on factors such as age, life expectancy, condition, and obsolescence.

· Depreciation: loss of value that has occurred over time based on factors such as age, life expectancy, condition, and obsolescence. If depreciation os recoverable, the amount is shown in these parenthesis (X). If depreciation is not recoverable the amount is shown in these parenthesis <X>

· Actual Cash Value: The estimated value of the item or damage at the time of loss. Generally, ACV is calculated as Replacement Cost Value (RCV) – Depreciation.

· Labor Minimum: The cost of labor associated with drive time, setup time and applicable administrative tasks required to perform a minor repair.

Your Estimate Summary:

For each type of coverage involved in your estimate there is a summary section that shows the total estimated cost (RCV and ACV) and the net claim amount for the coverage type.

· Line Item Total: the sum of all the line items for that particular coverage.

· Total Replacement Cost Value: The total RCV of all items for that coverage.

· Total Actual Cash Value: the total ACV of all items for that coverage.

· Deductible: the amount of the loss paid by you. A deductible is generally a specified dollar amount or a percentage of your policy limits.

· Net Claim: The amount payable to you after depreciation and deductible have been applied. This amount can never be greater than your coverage limit.

· Total Recoverable Depreciation: The total amount of depreciation you can potentially recover.

If you have a roof which has seen better days, call us for a complimentary inspection at:

402-281-2891.